13 Must-Know Important Financial Terms Before Borrowing Money

When was the last time you read a financial document and had no idea what all of the terms meant? If you are like most of us, it happens almost every time! If you’re thinking of starting or expanding a business, or wanting to make a large ticket purchase like a car or a home, borrowing money is often necessary. If you understand the ABC’s of borrowing money, it will transform you into a financially savvy and smart consumer.

Here are thirteen key financial words and terms that will assist you as you secure financing:

1. Amortization

Amortization is when you’re making equal periodic payments to pay down a balance. It is calculated to pay off the debt at the end of a fixed period, including the accrued interest, on the outstanding balance.

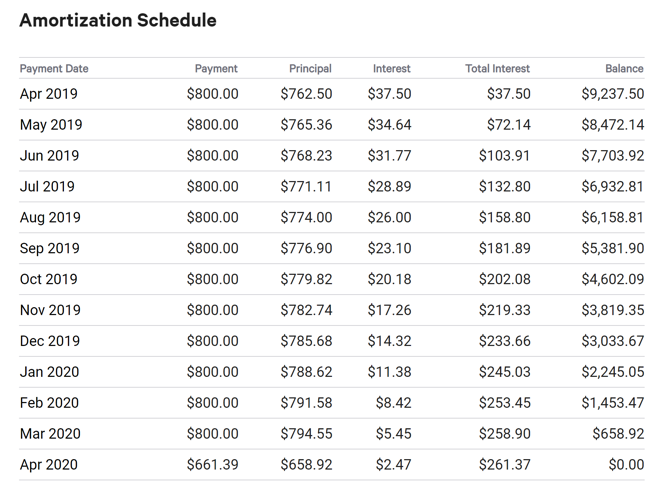

Example: Here’s an amortization schedule for a $10,000 loan with a 4.5% interest rate on a 12 month payment schedule.

Here is a handy amortization calculator.

Here is a handy amortization calculator.

2. Annual Percentage Rate (APR)

APR is an annual rate charged for borrowing money. It includes any fees or costs associated with the loan but it does not take compounding of interest within that year into account.

Example: If your loan has a APR of 10%, you would pay $10 per $100 you borrow annually.

3. Collateral

Collateral is an asset or property that the borrower offers to the lender as a way to secure the loan.

For example, when you request a large sum of borrowed money, a lender may be concerned that you may not be able to—or may choose not to—pay them back. As a result and a matter of security, they want you to put your car or a valuable asset down as collateral, so in the event that you cannot pay back the loan, you will have to surrender that particular asset.

4. Debt Consolidation

Debt consolidation—or consolidation as it is commonly known—allows borrowers to combine the account balances from multiple loans into a single loan to only make one monthly payment.

The borrower would first take a consolidation or personal loan, then use that money to pay off his or her existing loans. The consolidation loan typically has a more favorable interest rate or repayment term than the other existing debts and loans. Doing this combines, or as the name implies, consolidates, all of the borrower’s existing debt into a single loan. If you’re thinking about consolidating your debt, use a debt consolidation calculator to figure out if it’s beneficial for you.

5. Co-signer

A person who assumes responsibility on the loan, but who will not take a title interest in the property nor occupy the property.

Here’s where you have to be really careful. When you agree to be someone’s co-signer, you need to trust that the person you are getting into a loan agreement with is responsible. You would be liable for the aftermath if the other person fails to make payments or defaults.

6. Default

A failure to fulfill the repayment promise as specified in the loan agreement. In other words, you “default on a loan” when you no longer make regular payments on it.

7. Down payment

An initial payment of the total amount due to secure a loan.

For example, to take out a mortgage, lenders typically want to see you make a 20% down payment on the purchase price of the property before granting you a loan on the remaining 80%.

8. Lien

A lien is a legal claim or a right against property. Liens provide security, allowing a person or organization to take property or take other legal action to satisfy debts and obligations, similar to the term collateral. A lender’s claim to a borrower’s collateral is called a lien.

9. Line of Credit

A line of credit is a preset amount of money that your lender has agreed to lend you. You are able to draw from the line of credit when you need it, up to a predetermined maximum amount.

For example, if you were approved for a credit card with a credit limit of $10,000. You can immediately use the $10,000 on anything you wish. However, you do have to pay interest on that amount if you decide to use this line of credit past the payment period.

10. Loan Term

The period over which a loan agreement is in effect.

For example, a typical mortgage loan runs on a 15-year or 30-year term. Depending on the length of the loan term, there are various strategies and things to consider before making a decision. Consult with a mortgage loan expert to select the best option for you.

11. Maturity

Maturity is the date in which the term of the loan ends. In other words, it’s the final due date in which you must pay your loan off in full.

12. Principal

The original sum of money borrowed in a loan.

13. Refinancing

Refinancing is the process of replacing an existing loan with a new loan that typically has more favorable terms for the borrower on the newer loan. Note: refinancing should not be confused with Consolidation – where you are combining multiple loans into one single loan.

For instance, people typically refinance their mortgages so that they can reduce their monthly payments. By refinancing, they can often lower their interest rates, get a fresh mortgage term, and even change their loan agreement from one form to another—such as switching an adjustable rate mortgage to a fixed-rate mortgage.

Use a refinance calculator to determine whether it’s time for you to refinance your loans.

Bottom Line

Bottom Line

These basic financial terms should give you a general idea of what to look for and be aware of when you are borrowing money. If you have any specific questions, or if you need further clarification, you can always speak to a Empeople loan representative…we are always here to help! Lastly and most importantly, please remember never to sign for anything that you don’t fully understand.